02.08.2016 EU REFERENCE SCENARIO 2016 AND POLISH ENERGY MIX

The regularly published EU Reference Scenario is one of the European Commission's key analytical tools in the areas of energy, transport and climate action. It is updated by an external consultancy and predicts the impact of current EU policies on energy and transport trends, as well as changes in the expected amount of greenhouse gas emissions. The last update was published in 2013. The Reference Scenario provides projections for indicators, such as the share of renewable energy sources or levels of energy efficiency, on a five-year period up until 2050 for the EU as a whole and for each EU member state. The Reference Scenario is a projection of where EU current set of policies coupled with market trends are likely to lead.

Although the Reference Scenario is not designed as a forecast of what is likely to happen in the future, it provides a benchmark against which new policy proposals can be assessed, and is therefore of major importance to the new generation of EU policy measures to be published in the last quarter of 2016.

Please find below several key tables from the 2016 EU Reference Scenario for Poland with SOLIVAN’s comments.

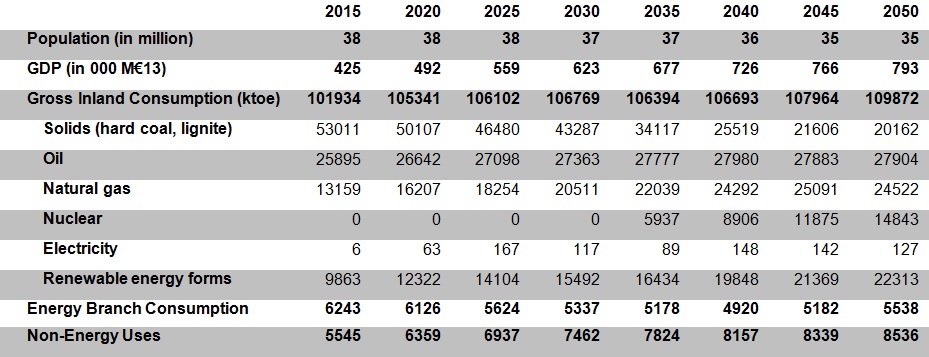

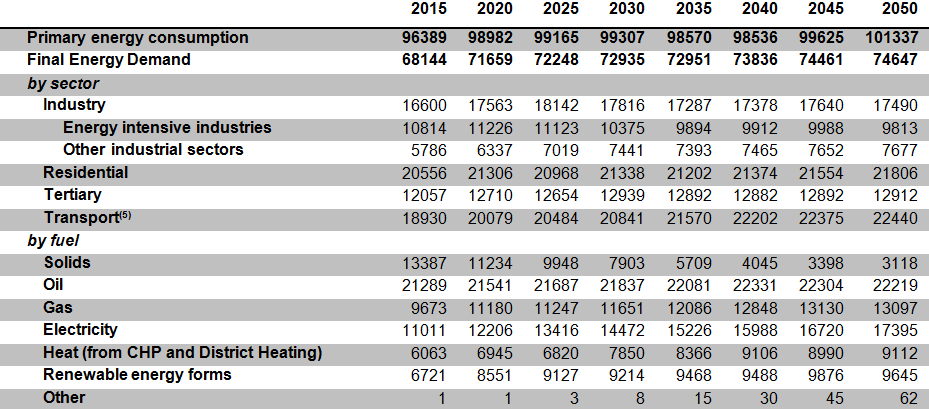

Table 1: Summary Energy Balance

Comment: The summary energy balance table indicates several remarkable assumptions. Firstly, a visible decline of energy production by hard coal and lignite after 2025 is forecasted, which relates to a significant de-commissioning obligation. So, it is not assumed that modernization of coal power plants can provide a remarkable life-time extension, and that a new fleet of coal power plants will be constructed.

Secondly, the role of natural gas for electricity production, especially as CHP plants, will significantly increase until 2050. So, capacity market mechanisms may rather provide support for peakload technologies, i.e. gas (combined cycle) power plants. Also, the role of biomethane as a supplement to natural gas may increase substantially.

Thirdly, it is expected that nuclear power will play a role from 2035 with significant growth until 2050. As nuclear is a baseload technology which will be financed through contracts for difference, the impact of capacity market mechanisms for new baseload investments will be limited, which is an indication that the current capacity market concept as presented by the Ministry of Energy will rather not be implemented to provide investments in coal firing capacity.

Finally, renewable energy production will grow between 10 and 20 percent every five years, although support will decrease, so those technologies become competitive even with limited support.

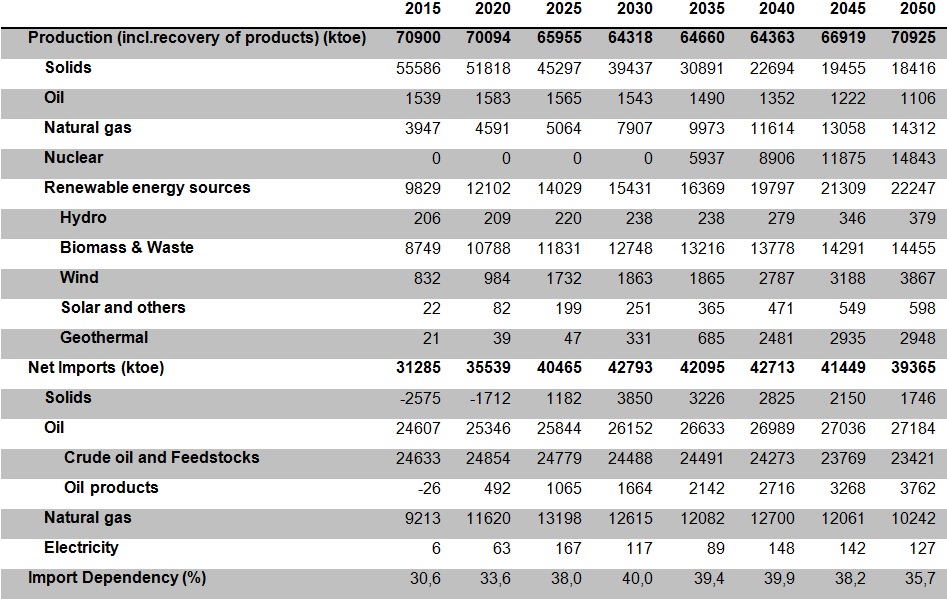

Table 2: Security of Supply

Comment: In addition to Table 1, the future development of renewable energy sources is presented in more detail, e.g., the increase of wind energy until 2020 is expected to be moderate whereas after 2020 a significant increase is expected, which indicates coming investments in offshore. Photovoltaic installations will face a remarkable growth until 2020, however, after 2020 it loses its speed to grow again after 2025. Geothermal will have a remarkable impact after 2025 – so, geothermal heat production will play an important role.

Furthermore, after 2020 the trade balance of solids, i.e. hard coal, will be negative, so that an increasing amount of hard coal will be imported, whereas until 2025 Poland will face an increase of natural gas imports, however after this date a decrease of natural gas imports is expected. This forecast may have an impact on the diversification of gas supply, i.e. the construction of a gas pipeline from Norway to Poland, which is one of the major topics for Poland’s energy independence strategy. According to this forecast, the economics of such undertaking might be questionable.

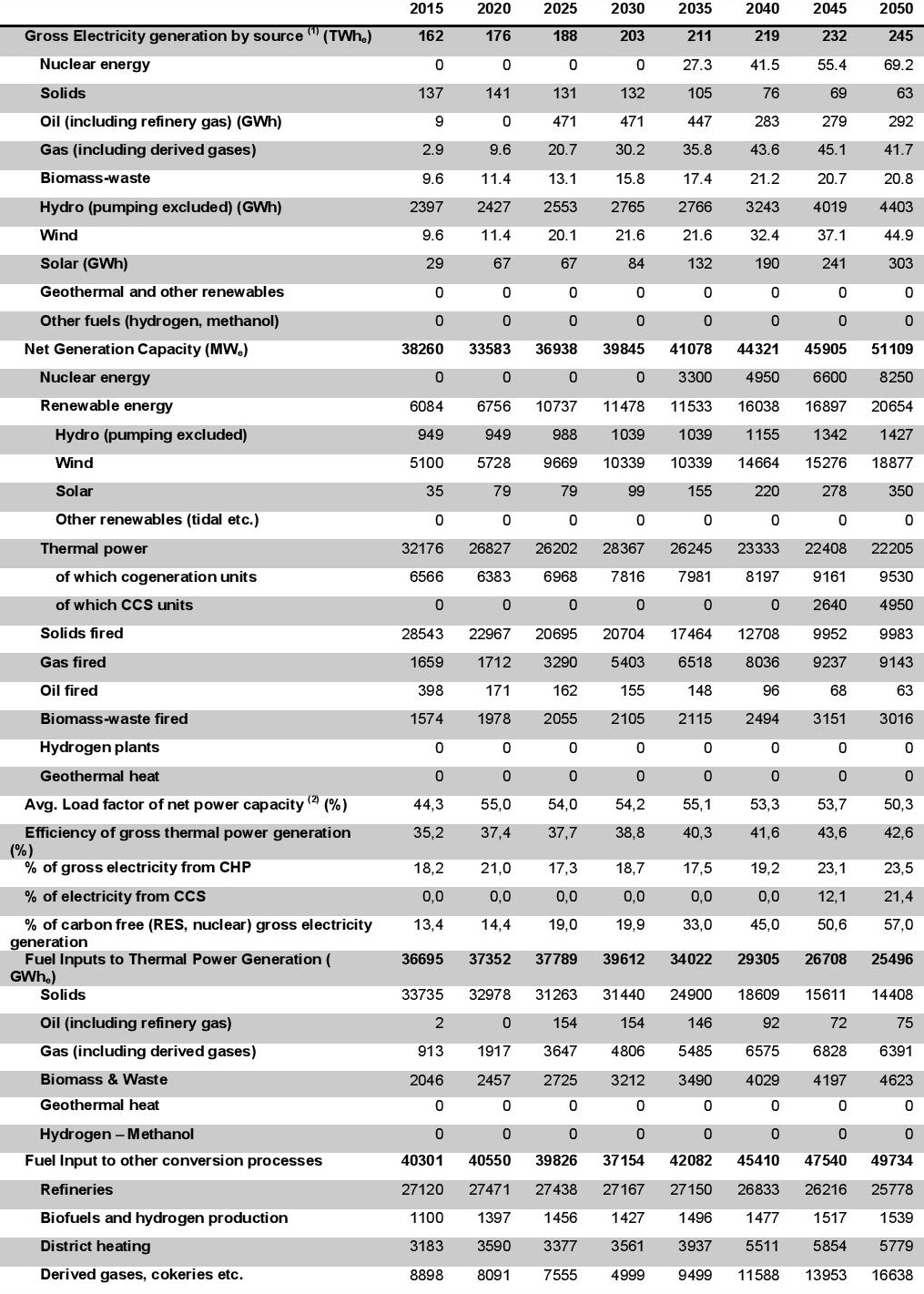

Table 3: Electricity

Comment: Poland is expected to face solid growth in gross electricity production from 162 TWh in 2015 to 245 TWh in 2050, with 14 TWh new electricity production until 2020, 12 TWh until 2025, and 15 TWh until 2030. After 2030, it is expected that nuclear will continuously take over the role of hard coal and lignite as base load technology. This is due to the de-commissioning of lignite power plants after 2030, which also has a large impact on the impact of solid fuels after 2030. The production curve of electricity by coal power plants provides the assumption that new investment will likely be seen within the next decade, however, after 2040 CCS technologies will deliver new coal fired production capacity – both nuclear and CCS require long-term contracts for difference to be financed.

However, electricity production by gas power plants will increase substantially - so, new EU capacity market design will clearly favor flexible technologies. After 2020, the amount of 1.6 GW new capacity and after 2025 the amount of 1.7 GW new gas power plant capacity is expected to be commissioned. Further growth after 2025 can be observed although less natural gas will be imported. So, either shale gas or biomethane may play an important role for the future of electricity production – however, it is unlikely that shale gas will become an acceptable technology from the environmental point of view, so biomethane and other derived gases seem to be the game changer.

Biomass and waste will face a solid but moderate growth until 2040 – however, the fuel input doubles within the next 30 years, and until 2020 remarkable growth by 400 MW new capacity is expected. Solar will reach grid parity after 2025 and will face remarkable growth during the next decades, but until 2025 the growth will be moderate. Wind will face a substantial growth of 9 TWh from 2020 to 2025, and another remarkable growth period after 2035. As due to the permitting procedures, the impact of offshore in the 2020-2025 growth will be limited, the major growth in production must be delivered by onshore wind. However, it is expected that this growth will stop after 2025 which provides the assumption that further development of onshore wind farms will be somehow limited by planning restrictions.

Furthermore, larger hydropower investments can be observed after 2035. New RES capacities to be on-grid in 2020 are presented as limited, so a further delay of the implementation of the auction system is expected. According to this table, growth of the renewable energy share in heat and transportation will allow Poland to fulfill its 2020 obligation, although this can be questioned and is currently being re-examined by the EU Commission. Therefore, it seems that the Ministry of Energy's approach starts to change, so the implementation of the auction system may speed up again to deliver new RES capacity earlier than forecasted.

Finally, the de-commissioning of coal power plants will have a negative impact on CHP and district heating for the next decade, but after 2030 CHP and district heating pick up again, so gas CHP plants and biomass and waste CHP plants will replace coal fired CHP plants slowly after 2020.

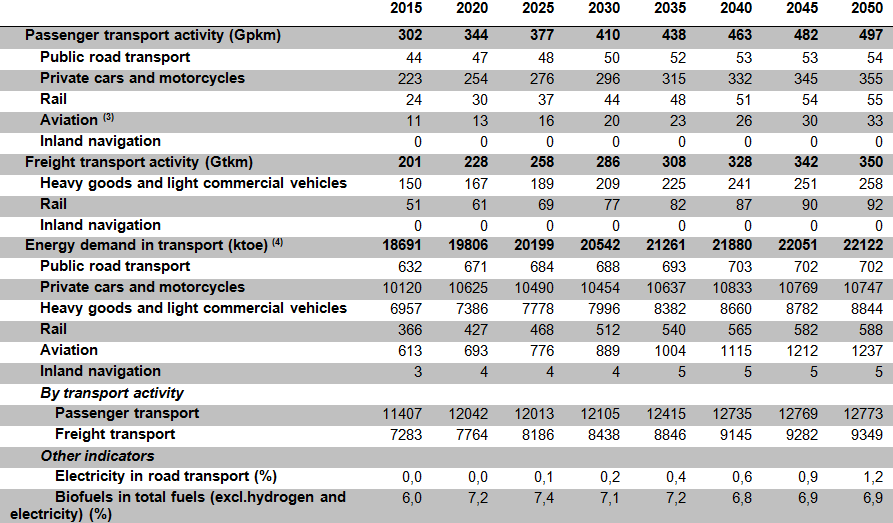

Table 4: Transport

Comment: This table provides a realistic view on the future of transportation. The impact of e-mobility in road transport is very limited – despite all recent political declarations. And biofuels will face growth only until 2020, but no further growth is expected after that date. So, biofuels will rather be used for electricity and heat production, especially to produce derived gases to be mixed with natural gas, than for road transportation.

Passenger and freight transport by rail and aviation will increase faster than public road transport, which is a clear indication that Poland should rather support its competitive rail transportation industry instead of supporting e-mobility. This might be less sexy, but seems to be more promising.

Table 5: Energy Efficiency

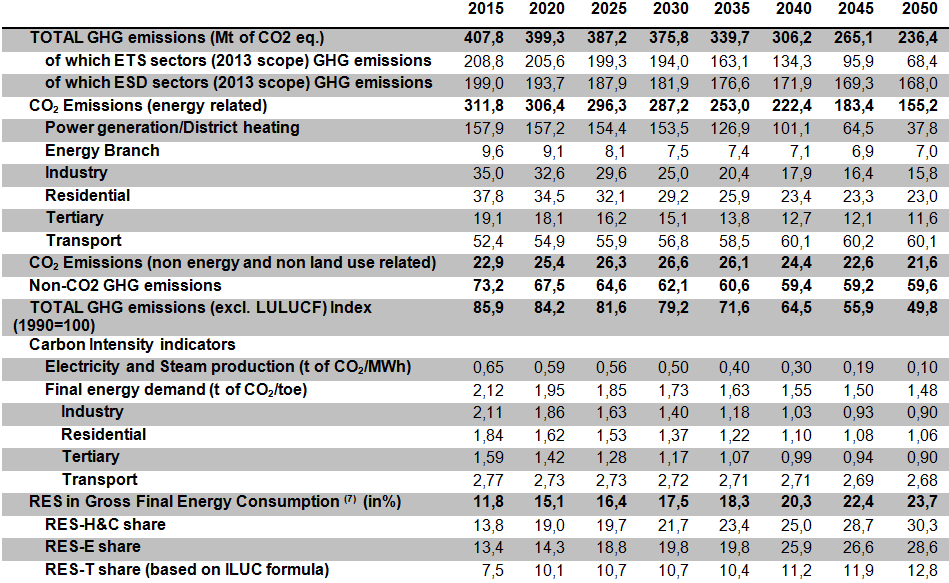

Table 6: Decarbonisation

Comment: Tables 5 and 6 demonstrate that although final energy demand faces a moderate increase decarbonisation speeds up. Furthermore, final energy demand provides evidence that the Polish economy further changes from energy-intensive industries to other industry sectors. The energy demand of transport picks up, whereas energy demand of residential and tertiary sector will rather stabilize. The role of hard coal and lignite as a fuel diminishes to a level of less than 25% in 2050 based on 2015 figures, whereas oil stabilizes, gas shows a moderate increase and renewables a remarkable increase. Derived fuels, i.e. electricity and heat, also grow remarkably. GHG emissions decrease by another 40% until 2050, with ETS-sectors having the major share in that decrease.

Power generation and heating are most addicted to GHG emissions reduction, and also industry and, less remarkable residential has its share. So, energy efficiency measures should pick up within the next decades to limit energy consumption. However, transportation faces a moderate growth of CO2 emissions although rail transportation increases its share, which puts a big question mark behind the predicted success story of e-mobility.

MINISTRY OF ENERGY WORKS ON AUTOCORRECTIONS TO THE REVISED RES ACT

The Ministry of Energy continues to work on further autocorrections to the revised RES Act, which entered into force on 1 July this year. In parallel, the notification of the RES support system continues.

For energy clusters and energy cooperatives, it is generally questioned whether an operative support system, such as the auction system, is an appropriate tool. Therefore, it is high likely that those auction baskets will stay empty for the time being, and investment support from EU grants will be available for energy clusters. According to the Ministry of Energy, clusters include electricity and heat production also by conventional fuels and its infrastructure, so a cluster hardly qualifies for the auction support system. To generally provide to higher capacity factors hybrid installations should achieve an extra basket. It is expected that a threshold of an amount of produced electricity exceeding the capacity factor of over 40% (3,504 MWh/MW installed capacity/year) will apply also to this basket. Of major importance will be whether the installed capacity or the connected capacity will be the relevant threshold. In case the installed capacity will count as threshold, onshore wind will team up with biogas and solid biomass installations to achieve the threshold. In case the threshold will be based on the connected capacity as of the grid connection agreement, onshore wind will team up with PV to achieve the threshold.

Furthermore, it is under discussion whether the local biomass obligation, which according to current wording from 1 January 2018, will apply to agricultural biomass and also to forest biomass. Furthermore, the obligatory minimum share of agricultural biomass will be cancelled. This will have a major impact on the future fuel mix of larger biomass installations.

Finally, the extension of net-metering for installations with up to 200 kW installed capacity is discussed. Currently, only installations up to 40 kW are subject to net-metering. As currently only private persons and farmers are benefiting from net-metering, it is under discussion whether also entrepreneurs may apply for net-metering of their power producing installations.

VOLUME FOR 2016 AUCTIONS TO BE PUBLISHED SOON, BIOGAS AND PV FAVORED

By the end of August 2016 the volume for the 2016 auctions will be published. Currently, the Ministry of Energy has already finished a draft regulation, however, this draft regulation has not yet been published. Due to the fact that the notification will most likely still be pending when 2016 auctions will take place, those auctions should be understood as test auctions for installations with up to 1 MW installed capacity. However, it provides an indication which technologies are favoured. The total volume for 15 years amounts to 4.1 TWh, whereas a maximum of 1.57 TWh will be dedicated for “other installations” not exceeding the capacity factor of over 40% (3,504 MWh/MW installed capacity/year). So, the general auction volume equates to 273 GWh/year, whereas 40%, i.e. 109 GWh, are dedicated to installations with low capacity factors. This equates to 30 MW of biogas installations with 5,000 FLH and to one hundred 1 MWp ground-mounted PV farms or about thirty 1 MW wind turbines, alternatively. So, in case the reference price will be sufficient for small wind turbines they may take over this basket, or otherwise PV installations will succeed.

The Ministry of Energy has already made a clear statement that they expect new PV installations to bridge summer power production gap, so the reference price for small wind turbines may substantially decrease and amount to less than PLN 350 per MWh to avoid competition for PV, and in consequence the reference price for large wind turbines (for 2017 auction) may amount to less than PLN 320 per MWh.

WIND TURBINE INVESTMENT ACT TO BE CHANGED

The Wind Turbine Investment Act, which entered into force on 15 July, might be subject to substantial changes after increasing pressure from the EU Commission and international investors – the Ministry of Energy is responsible. Under the WTI Act, the minimum distance between wind turbines between residential and protected landscape areas, etc. is 10H, i.e. 10 times tip height – similar to the Bavarian approach, but with the important difference being that the Polish regulation also applies in case a master plan has been established. This may change to a 5H obligation in case the municipality council appropriately adopts a master plan.

Furthermore, a certification obligation (being subject to notification) may finally be implemented, however, in this case technical elements of the wind turbine will no longer state a building structure being subject to supervision by the building supervision authorities. This qualification of technical elements as a building structure would provide to a broadly criticized and legally questionable real estate tax increase for wind turbines, which according to authors of the WTI Act was not intended.

Nevertheless, we recommend cautiously observing non-officially proposed changes and legislation process, as the recent experience has proven that this topic is highly political and sudden legislation pitfalls are possible at any moment.